U.S. treasury securities, which come in bills, notes, and bonds depending on their maturity, are considered some of the safest and most reliable investments and have the following advantages over other types of bonds:

- Liquidity: Treasury securities are extremely liquid, and part of the reason is that the Treasury market is one of the world's biggest bond markets. So you can buy and sell them at will.

- Terrific “call protection”: The Treasury cannot call, or buy back, any bonds before their maturity date.

- Taxes: Treasury securities are not subject to state or city taxes.

- Book-entry form: If you buy Treasury securities, you are not issued pieces of paper that can be lost, destroyed, etc. Instead they are held in book-entry form. Any bond that you buy is held directly in the TreasuryDirect system run by the Bureau of Public Debt or in financial institutions'/brokers' book-entry systems.

The face value on Treasury securities is $1,000, and therefore that is the minimum investment. Investors can choose among the following types of government fixed income securities:

- Treasury bills: These securities feature the fastest maturities—13, 26, and 52 weeks—and are considered as liquid as cash. Along with no credit risk, they also have minimal interest rate risk because they mature so quickly.

- Treasury notes: These securities mature between 2 and 10 years, which means that there is more interest rate risk and that their prices rise and fall more than Treasury bills.

- Treasury bonds: These securities feature maturities between 10 and 30 years.

- Zero-coupon Treasury securities: Also known as strips, these securities are the most volatile.

Federal Agency Bonds

Federal agencies in the U.S. issue a massive amount of debt—in the trillions of dollars. When agencies like the Federal Home Loan Mortgage Corporation (Fannie Mae) and the Federal Home Loan Banks (FHLBs) issue bonds, they are backed by either a government guarantee or a moral guarantee. These bonds are generally considered to have little or no credit risk and they pay out just slightly more interest than Treasury securities. Also, they can be called back by the agencies that issued them before their maturity date.

Federal Home Loan Mortgage Corporation (Fannie Mae)

Created by the federal government in 1938 to provide extra money for mortgage lenders in the middle of the Depression, Fannie Mae has been a privately held company since 1968. It is one of the biggest issuers of debt securities in the world.

Federal Home Loan Banks

The federal government manages 12 regional Federal Home Loan Banks which are technically owned by the U.S. savings and loans (S&L) institutions. These banks are in business to lend money to the S&Ls if they need it. Their securities offer a fixed interest rate and can be called back by the agencies that issued them before their maturity date. Denominations range from $10,000-$500,000.

Federal Farm Credit Banks

The federal government manages the Federal Farm Credit System which is technically owned by the 37 farm banks in the group. These banks provide farmers and cooperatives with loans when they need them. Minimum investment for short-term debt is $50,000. Longer-term debt requires just a $1,000 minimum.

Ginnie Maes

Ginnie Maes are mortgage pass-through securities from the Government National Mortgage Association (GNMA), which is a division of the Department of Housing and Urban Development. The GNMA itself does not issue Ginnie Maes, but insures the securities which are guaranteed against default. Ginnie Maes are formed by grouping mortgages insured by the Federal Housing Administration and the Veterans Administration. Investment bankers securitize the mortgages, generating bonds. The bank then receives a servicing fee that runs to half a percentage point. Mortgage holders pay their mortgages and that interest is passed to the bank who pays the bondholder monthly interest and principal payments. Ginnie Maes securities have some major disadvantages:

- State income taxes are imposed on any interest earned.

- Maturity dates are uncertain since homeowners refinance mortgages when interest rates fall.

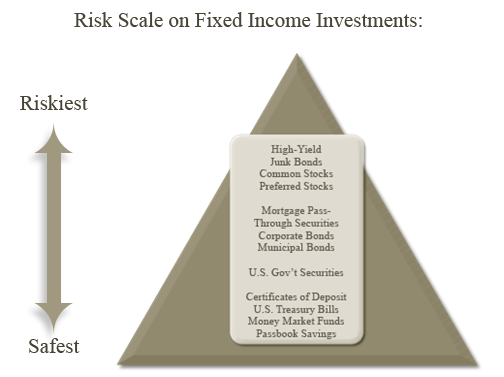

Municipal Bonds

Bonds issued by states, counties, and other state divisions to fund the building and maintenance of public services and other facilities (highways, airports) are known as municipal bonds. They can be called back by the agencies that issued them before their maturity date.

Corporate Bonds

Basically just loans from investors to corporations, corporate bonds feature many variables to take into consideration:

- Price: Connected to the bond's liquidity, seniority, credit rating, call features, covenants, and event risk.

- Structures: Senior notes, subordinated debentures, and convertible bonds.

- Rates: Some corporate bonds are sold with floating interest rates.

U.S. Government Series EE Bonds

These cash investments offer investors relatively high interest rates and terrific tax advantages. They are also known as savings bonds.

Features of Series EE Bonds:

- You can buy them at 50% of the face amount

- Face value ranges from $50 to $10,000

- One person can buy a maximum of bonds equaling $30,000 in face value annually

- If you hold the bonds for a minimum of five years, they increase in value

- You cannot redeem any series EE bonds until after you have held them for six months

- Interest is exempt from state and local taxes

- You will not have to pay federal taxes on any earnings until you redeem the bonds

- If you use bond earnings to pay for qualified education expenses (your adjusted gross income must be lower than the stated levels), you may be able to avoid paying federal taxes on any interest income

What Percentage of Your Portfolio Should be in Bonds? You should always hold some bonds in your portfolio—the amount will depend on how old you are, your tolerance for risk and the length of time left until you retire. If you are older, the proportion of bonds that you are holding should be closer to your age so that you lower the percentage allocated to equities (which tend to have higher risk) in your portfolio.

What Percentage of Your Portfolio Should be in Bonds? You should always hold some bonds in your portfolio—the amount will depend on how old you are, your tolerance for risk and the length of time left until you retire. If you are older, the proportion of bonds that you are holding should be closer to your age so that you lower the percentage allocated to equities (which tend to have higher risk) in your portfolio.

Fixed Income Best Practices