It is imperative that portfolio managers’ performance be periodically assessed. This is necessary to determine whether to make management changes if the portfolio is failing to meet its goals and/or the money managers are not performing in line with their peers.

Performance is measured by calculating the return for portfolios over a specified period of time. Performance evaluation explores whether the manager outperformed the set benchmark (also known as the standard) and how the manager achieved portfolio returns.

Three single-index methods calculate money managers’ performance:

Treynor Index:

- Measures extra return per unit of risk.

Sharpe Index:

- Measures extra return in relation to variability.

Jensen Index:

- Utilizes a special asset pricing model.

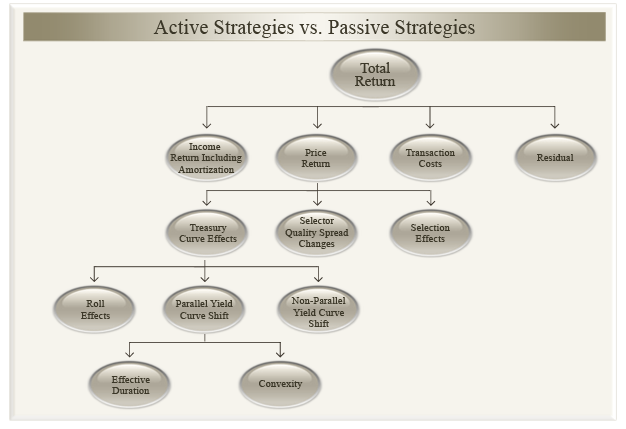

Return attribution analysis is the method used to figure out the decisions made by the manager that led to the returns achieved.

Fixed Income Best Practices